ARM Processor Licensing Revenue Up 42%

ARM HOLDINGS PLC REPORTS RESULTS FOR THE SECOND QUARTER AND HALF YEAR ENDED 30 JUNE 2014

A presentation of the results will be webcast today at 09:30 BST at www.arm.com/ir

CAMBRIDGE, UK, 22 July 2014 ARM Holdings plc [(LSE: ARM); (NASDAQ: ARMH)] announces its unaudited financial results for the second quarter and half year ended 30 June 2014

* Normalised figures are based on IFRS, adjusted for acquisition-related charges, share-based payment costs, restructuring charges, Linarorelated charges, share of results of joint venture, intangible amortisation, impairment of investments, and exceptional items. For reconciliation of IFRS measures to normalised non-IFRS measures detailed in this document, see notes 12.8 to 12.11.

** Net cash generation is defined as movement on cash, cash equivalents, short-term and long-term deposits, adding back dividend payments, investment and acquisition consideration, other acquisition-related payments, share-based payroll taxes, investment in joint venture, payments to Linaro, cash outflow from exceptional IP indemnity and similar charges and deducting inflows from share option exercises see

notes 12.3 to 12.7.

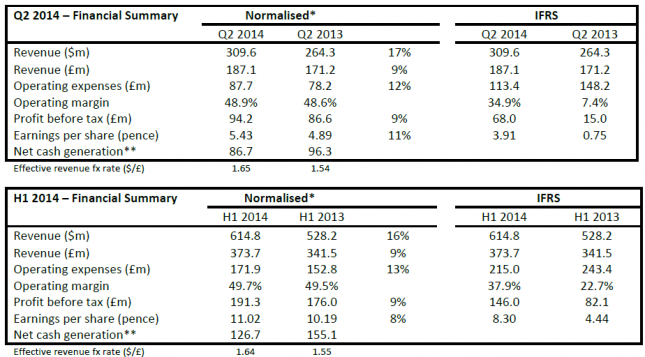

Q2 financial summary

- Group revenues in US$ up 17% year-on-year ( revenues up 9% year-on-year)

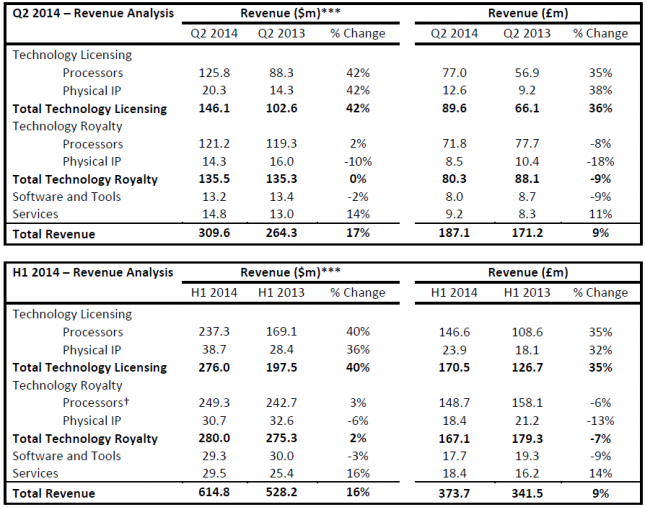

- Processor licensing revenue in US$ up 42% year-on-year

- Processor royalty revenue in US$ up 2% year-on-year

- Normalised profit before tax and earnings per share up 9% and 11% year-on-year respectively

- Net cash generation of 86.7m

- Interim dividend increased by 20%

Progress on key growth drivers in Q2

- Growth in adoption of ARM technology

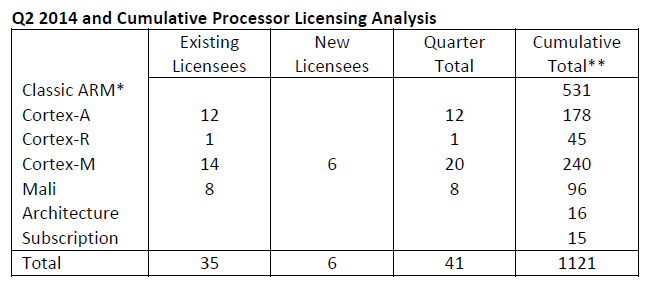

- 41 processor licences signed across our target markets of mobile computing, consumer electronics and embedded intelligent devices, taking the cumulative number of licences signed to more than 1,100

- Advanced technology enables a higher royalty percentage per chip in mobile devices, consumer electronics and enterprise infrastructure

- 7 ARMv8-A processor licences signed, including lead licences for next generation designs

- 8 Mali multimedia processor licences signed, including first licences for video and display processors

- Growth in shipments of chips based on ARM processor technology

- 2.7 billion ARM-based chips shipped, up 11% year-on-year

- Shipment growth especially strong in enterprise networking and microcontrollers

Outlook

ARM enters the second half of the year with a healthy pipeline of opportunities that is expected to both underpin continued strong licence revenue and give rise to an increase in the level of backlog. Market data indicates improving semiconductor industry conditions, leading to the expectation of an acceleration in royalty revenue growth in H2 2014. Given these dynamics, we expect Group dollar revenues for full year 2014 to be in line with market expectations.

Simon Segars, Chief Executive Officer, said:

Our continued strong licensing performance reflects the intent of existing and new customers to base more of their future products on ARM technology. The 41 processor licences signed in Q2 were driven by demand for ARM technology

in smart mobile devices, consumer electronics and embedded computing chips for the Internet of Things, and include further licences for ARMv8-A and Mali processor technology. This bodes well for growth in ARMs medium and long term royalty revenues.

As expected, our royalty revenue in Q2 2014 has been impacted by seasonal trends and inventory management in parts of the electronics supply chain. An improving market environment in the second half gives us confidence in strengthening royalty revenue in H2 2014.”

*** Dollar revenues are based on the Groups actual dollar invoicing, where applicable, and using the rate of exchange applicable on the date of the transaction for invoicing in currencies other than dollars. Over 95% of invoicing is in dollars.

Includes a deduction, recognised in Q1 2014, of $5 million for prior years royalties over-reported to ARM by a customer.

Financial review

(IFRS unless otherwise stated)

Total revenues

Total dollar revenues in Q2 2014 were $309.6 million, up 17% versus Q2 2013. Q2 sterling revenues of 187.1 million were up 9% year-on-year.

Half-year dollar revenues in 2014 amounted to $614.8 million, up 16% on H1 2013.

Licence revenue

Total dollar licence revenues in Q2 2014 increased by 42% year-on-year to $146.1 million, representing 47% of Group revenues. Licence revenues comprised $125.8 million from processor licences and $20.3 million from physical IP licences.

Group order backlog at the end of Q2 2014 was down about 10% sequentially. It is expected that the licensing opportunity pipeline, including potential subscription licences and opportunities for more licences of ARMs next generation processors, will give rise to an increasing level of backlog in the second half.

Royalty revenues

Total dollar royalty revenues in Q2 2014 were up slightly on Q2 2013 at $135.5 million, representing 44% of Group revenues. Royalty revenues comprised $121.2 million from processors and $14.3 million from physical IP. Processor royalty revenues increased 2% year-on-year. Industry revenues were up 5% over the relevant shipment period (i.e. Q1 2014 compared to Q1 2013).

ARMs royalty revenues in Q2 2014 were impacted by ongoing inventory management in consumer electronics, for example operators selling off older 3G handsets ahead of switching subsidies to LTE handsets. ARM expects to outperform the overall semiconductor industry in H2 2014 as more chips are sold to OEMs building more advanced devices, which typically utilise more ARM technology.

Other revenues

Sales of software and tools in Q2 2014 were $13.2 million, a decrease of 2% year-on-year. Service revenues were $14.8 million in Q2 2014, up 14% year-on-year. Together revenues from software and tools and services represented 9% of

Group revenues.

Gross margins

Normalised gross margins in Q2 2014 were 95.8% compared to 95.6% in Q1 2014 and 94.3% in Q2 2013.

Operating expenses and operating margin

Normalised income statements for Q2 2014, H1 2014, Q2 2013 and H1 2013 are included in notes 12.8 to 12.11 below which reconcile IFRS to the normalised non-IFRS measures referred to in this earnings release.

Normalised operating expenses were 87.7 million in Q2 2014 compared to 84.3 million in Q1 2014 and 78.2 million in Q2 2013. Normalised operating expenses in Q2 2014 included a charge of 2.7 million relating to the revaluation of monetary items due to changes in foreign exchange rates, and the impact of a weaker dollar on the accounting for derivative instruments. Normalised operating expenses in Q3 2014 (assuming effective exchange rates similar to current levels) are expected to be in the range 90-92 million as we continue to invest in our research and development teams and in our business infrastructure.

Normalised operating margin was 48.9% in Q2 2014, compared to 50.4% in Q1 2014 and 48.6% in Q2 2013.

Normalised research and development expenses were 39.7 million in Q2 2014, representing 21% of revenues, compared to 39.8 million in Q1 2014 and 37.2 million in Q2 2013. Normalised sales and marketing expenses were 19.8 million in Q2 2014, being 11% of revenues, compared to 20.4 million in Q1 2014 and 17.8 million in Q2 2013. Normalised general and administrative expenses were 28.2 million in Q2 2014, representing 15% of revenues, compared to 24.1 million in Q1 2014 and 23.2 million in Q2 2013.

Total IFRS operating expenses in Q2 2014 were 113.4 million (Q2 2013: 148.2 million after exceptional IP and indemnity charges of 41.8m) including share-based payment costs and related payroll taxes of 14.3 million (Q2 2013: 15.7

million), a restructuring charge of 8.4 million (including 3.4 million in respect of accelerated share-based payment charges) (Q2 2013: nil), and amortisation of intangible assets, other acquisition-related charges, impairment of investments and Linaro-related charges of 3.0 million (Q2 2013: 12.5 million). The restructuring charge of 8.4 million follows a review of the skills and capabilities across the business during which approximately 130 people left the Group.

We are reinvesting in new skills and capabilities to further strengthen the organisation for future growth. We finished the first half having grown net headcount by 211 employees.

Total share-based payment costs and related payroll tax charges of 14.8 million in Q2 2014 were included within cost of revenues (0.5 million), research and development (9.8 million), sales and marketing (2.4 million) and general and

administrative (2.1 million).

Earnings and taxation

Normalised profit before tax in Q2 2014 was 94.2 million compared to 86.6 million in Q2 2013. After including acquisition-related and share-based payment costs, intangible amortisation, restructuring charges and share of results of

joint ventures, IFRS profit before tax was 68.0 million in Q2 2014 compared to 15.0 million in Q2 2013.

The Group’s effective normalised tax rate was 18.3% in Q2 2014 (IFRS: 18.4%). ARMs full-year normalised effective tax rate in 2014 is expected to be slightly below 18%.

In Q2 2014, normalised fully diluted earnings per share were 5.43 pence (27.83 cents per ADS[1]) compared to 4.89 pence (22.23 cents per ADS) in Q2 2013. IFRS fully diluted earnings per share in Q2 2014 were 3.91 pence (20.06 cents per ADS) compared to earnings per share of 0.75 pence (3.41 cents per ADS) in Q2 2013.

Balance sheet

Intangible assets at 30 June 2014 were 603.4 million, comprising goodwill of 520.7 million and other intangible assets of 82.7 million, compared to 525.9 million and 82.9 million respectively at 31 December 2013.

Total accounts receivable were 122.4 million at 30 June 2014, compared to 136.2 million at 31 December 2013.

Cash flow and interim dividend

Net cash generation in Q2 2014 was 86.7 million. Net cash at 30 June 2014 was 746.4 million compared to 706.3 million at 31 December 2013.

In respect of the year to 31 December 2014, the directors are declaring an interim dividend of 2.52 pence per share, an increase of 20% over the 2013 interim dividend of 2.1 pence per share. This interim dividend will be paid, out of the UK GAAP distributable reserves of ARM Holdings plc, on 3 October 2014 to shareholders on the register on 5 September 2014.

In February 2014, the Board indicated that it intended to continue to maintain a flat share count over time by undertaking a limited share buyback programme. In this context, the Group bought back 1.4 million shares in Q2 at a total cost of 12 million.

[1] Each American Depositary Share (ADS) represents three shares.

Technology Licensing

Processor licensing

41 processor licences were signed in Q2 2014, higher than ARMs normal licensing run rate and reflecting the strong demand for ARMs latest technology.

Twelve of the licences signed were for ARMs Cortex-A series processors, mainly for use in smartphones, tablets and other consumer electronics devices. Seven of the licences were for processors based on the ARMv8-A architecture, including the first two lead licences for ARMs next generation Cortex-A processors. To date, ARM has signed a total of 50 ARMv8-A processor and architecture licences which typically command a higher royalty compared to previous generations of ARM technology.

ARM also signed eight licences for its Mali multimedia processors, for use in mobile and consumer electronics, and in embedded computing applications such as point-of-sale systems. The Mali graphics processor product line has been extended to include video and display processors, and two of the eight licences were for these new technologies.

Twenty of the licences signed in Q2 were for Cortex-M class processors for use in technologies required for the Internet of

Things; microcontrollers, smart sensors and low-power wireless communication chips.

* Includes ARM7, ARM9, ARM10 and ARM11

**Adjusted for licences that are no longer expected to generate royalties

Physical IP licensing

ARMs physical IP is used by fabless semiconductor companies to implement their chip designs. Platform licences are royalty bearing licences that enable foundries to manufacture chips using ARMs physical IP. Each foundry requires a

platform licence for each process node. ARM has signed more than one hundred platform licences with leading foundries, from 250nm to 14nm.

During the quarter we signed a platform licence with a leading foundry at 55nm. ARM now has physical IP agreements with four foundries at the 55nm node, the smallest geometry with general purpose embedded flash, which is a

requirement for many embedded and Internet of Things applications.

In Q2 we saw strong licence revenue growth as we achieved engineering milestones, on licences signed in previous quarters, for technologies including 20nm and 16/14nm physical IP.

The Full press release can be found here.